A whitepaper by EthosData Virtual Data Room

Assessing the impact of Covid-19 on M&A

Covid-19 has changed every aspect of life – the way we interact, work, consume, spend our free time and contribute to the economy. As with so many parts of the global economy, merger and acquisition activity has undergone a major shift. As businesses turn their attention to the immediate threat and need for recovery, some deals are being cancelled, while others are being tabled. However, we are seeing a wave of new deals as a result of the ongoing crisis, as some companies rush to restructure and find liquidity.

After a decade-long period of record dealmaking, global merger and acquisition activity plummeted 28% in the first quarter of 2020 to its lowest level since 2016, as reported by Reuters. US-based deals dropped by half on the comparative 2019 period to $252 billion, according to data from Refinitiv. Dealmaking in China, where the first cases of Covid-19 were identified, also took a dive. China-target M&A halved in value, year-on-year in the first quarter of 2020, while Chinese outbound was down 85%, the lowest level since 2004.

Europe was the exception, emerging from the first quarter unharmed as deal volume rose by $232 billion. This was largely thanks to several large-volume transactions completed just before the Covid-19 crisis ramped up, including insurance broker Aon’s $30 billion takeover of rival Willis Towers Watson.

As results from the end of April are made public and the full picture starts to come into sharper view, we are likely to see the deep impact this unprecedented event is having. But we are now just weeks into what is likely to be a lengthy process and recovery spanning years. With most financial hubs like London, New York, Mumbai and Paris under near total lockdown, the year-on-year figures are likely to be impacted further.

The toll on financial markets is difficult to grasp, and becomes more significant every day. Global GDP is anticipated to fall 2.4% this year, with the US and Eurozone contracting 5.2% and 7.3%, respectively, according to data from S&P Global.

We are in uncharted territory. Companies who were, just months ago, considering a merger or acquisition to grow, are now trying to understand what the future may bring. Ensuring liquidity remains top of mind, along with a need to protect themselves, their workforce and their future prospects. But current global restrictions are making the traditional M&A process impossible. As one banker told Barrons, “How can you sell a company if you can’t look the buyer in the eye?”

While new ‘traditional’ acquisitions are broadly on standby, EthosData is seeing some new, fast-paced fundraising and restructuring taking place. We are also seeing similar levels of user activity within our data room, and existing deals are moving forward, albeit at a slower pace than in relatively ‘normal’ circumstances. There are now countless obstacles for businesses midway through acquisition. These include valuation gaps, cash flow concerns, access to funding and the inability to meet with advisors and investors face-to-face.

While new ‘traditional’ acquisitions are broadly on standby, EthosData is seeing some new, fast-paced fundraising and restructuring taking place.

Lessons from the past: what could happen next?

As we have seen in the past few weeks, it’s impossible to know for certain how this unprecedented healthcare crisis will pan out, and improve to a point where the global financial economy can start playing catch-up.

However, we can look back to two comparable periods in history to try and obtain some idea of how and when the world’s economy, and with it M&A activity, might be revived.

The Spanish Flu outbreak

First recorded in 1918, the disease infected around a third of the global population, and killed up to 50 million people, as the last real pandemic of this kind.

Historians find it difficult to agree on an exact figure of the economic impact of the Spanish Flu outbreak given its proximity to the end of the First World War and the heavy costs associated with this.

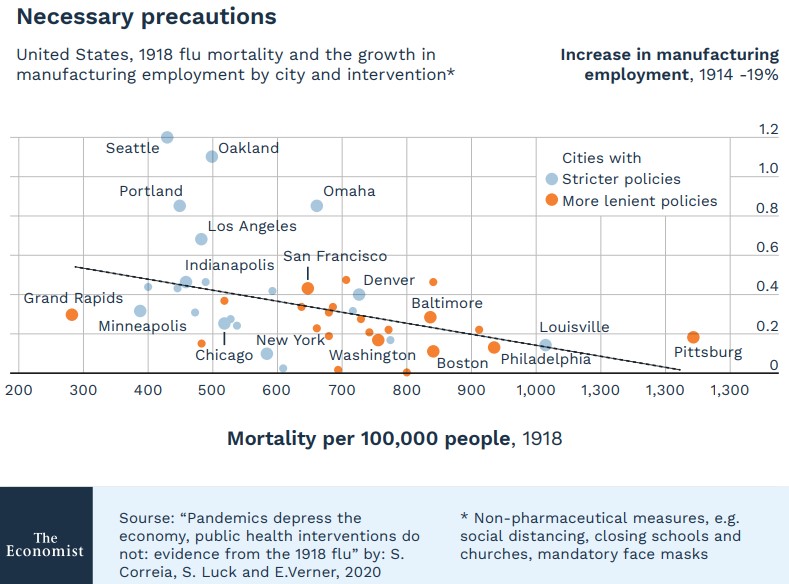

But there are lessons we can learn from this crisis, in particular the impact that social distancing rules had on the workforce and economy. The major industry in many cities observing these rules, manufacturing, saw a spike in activity and employment in the following years.

Cities which implemented early and extensive non-pharmaceutical interventions, such as social distancing, suffered no adverse economic effects over the medium term. This was illustrated by a study from three economists earlier this year, Pandemics Depress the Economy, Public Health Interventions Do Not: Evidence from the 1918 Flu.

This could be a positive sign for countries currently observing social distancing rules. If the results are parallel to those felt by the Spanish Flu, global economies following strict social distancing rules will likely recover faster than those which have elected not to introduce any such precautions and with increased economic activity we should see an increase in the number of M&A transactions.

Global recession

If we go back to the 2008 global recession, we are able to look in more detail at the impact in M&A activity. M&A was hard-hit during the period, left reeling from the fallout and consequential concerns about the strategy being ‘too risky’, as well as a lack of liquidity. This led to a five-year spell of many companies choosing to focus on cost-cutting and organic growth, rather than acquisitions.

For the activity taking place in the immediate aftermath of the recession, it was a story of two halves. Many deals became fast-firing with an intense need for closure, while others morphed into incredibly long, drawn out processes which closed looking nothing like the deal they had originally been intended for. For example, IPOs moved to full-asset sales to sell-offs of small company branches – there was a sense of uncertainty and fear around the trade.

The introduction of new regulation, pricing fluctuation and nervousness on the parts of investors and sellers meant the industry found it tough to get back onto its feet.

The tide did turn though. Companies began re-introducing acquisitions to their growth strategies, while private equity funds raised huge sums of money to deliver investments, and the markets responded positively – which in turn, saw a marked increase in demand for our data-room service. Dealmakers needed the speed and security our top platform and experienced team provides.

This culminated in a return to favour for M&A, and from 2013 investors “rewarded buyers with positive announcement returns—a major departure from the historical pattern,” according to an observation from the Boston Consulting Group in its 2018 M&A report.

Acquisitions continued to gain popularity and until recently, achieved great growth. Dealogic reported that in 2018, advised volumes reached $ 3.35 trillion, the highest level since the record-breaking 2015, in which $3.63 trillion was recorded. It is a positive sign that within what was arguably its toughest decade to date, M&A was once again reaching uncharted realms of success within seven years.

The global recession and Spanish Flu epidemic are the two most relatable parallels to the situation we find ourselves in today, and while each took very different paths to recovery, both give us reasons to be positive about the future of the M&A industry.

It is difficult to say currently whether we will see a V, a U or a tilted L-shaped recovery. Experts may not be able to agree on the kind of recovery we will experience, but we are sure that after the initial shaky period of indeterminate length, we will see a significant uptick in M&A of all kinds – even in the least positive scenario.

However as we sit in the middle of this unique situation, the timeline we are working within is uncertain, and the backdrop we are working against even more so. There are many factors that make it a shaky ground to build on. These include the impact of Covid-19 itself, the potential increased regulation to avoid foreign ownership in strategic industries or concentration in key sectors, the change in nature of the state as supporter and owner of companies, and the political pressures of the US elections, Brexit among others.

How could the crisis impact the M&A space in the long term?

The immediate shocks will be followed by longer ranging issues which will unfold over the coming years. These will be largely driven by a real shift in human behaviour, the impact seen not only in the M&A sector, but across the wider consumer market, thanks to many of the current restrictions in movement.

Which sectors are likely to see a rise in M&A?

from the general public in what constitutes ‘safe’ shopping and travel. It is likely that many will simply feel safer in the comfort of their own homes.

To this end, traditional high street retailers may look to quickly expand their online presence by snapping up complementary ecommerce players. This way, these brick-and-mortar retailers can hedge risk by expanding their distribution channels online and/or relocate inventory. This will likely drive up the price and interest in attractive and flexible ecommerce providers.

During the second half of Q2 2020, we expect to see an uptick in activity which will be broadly driven by strategic and opportunistic M&A and restructuring. Opportunities will be found in sectors such as travel, oil, tourism, retail and leisure which currently find stocks prices tumbling, whereas healthcare and food firms are seeing interest piqued. Cash-rich buyers will move fast; and we’ll likely see activity from those willing to spend quickly, from corporations to private equity.

How might deal processes change?

Some urgent and straightforward deals will be completed faster; but other more complex deals such as complex asset sales, carve outs or portfolio sales may take a longer time to complete. Rather than large, costly sell-offs, firms in need of instant liquidity may choose to sell single, underperforming and costly arms of business to the highest bidder. These sell-offs will not wait around, as their needs move from lengthy negotiations over price to a desire to sell fast to avoid a short term disaster.

The due diligence process is likely to undergo changes, as there may well be provisions for this kind of global emergency which become included and checked as standard.

New amendments, emergency planning procedures, insurance quotes and cancellation options could suddenly become commonplace in the most straightforward of agreements. Firms will likely be doing everything they can to cover themselves for either the next Covid-19 wave, or a future crisis which could plunge the sector, and wider economy, into chaos.

Regulatory requirements around employee safety, remote working and short-term working proposals may all have to be adhered to and considered for each deal. Finally, as working remotely becomes more commonplace, close attention will need to be paid to who is able to access sensitive data, information which could impact markets, and files which have no business being in the public domain. Working remotely has become more commonplace, and even after the worst of this pandemic has passed, it is likely that it will be here to stay in some form. The need for tools to keep transaction data secure, and to make transactions simpler, will only grow further. Data rooms will become a vital part of each deal, and their functionality may evolve to facilitate other areas of the transaction Partnering with a trusted, established player in the data room field will be more essential than ever.

New amendments, emergency planning procedures, insurance quotes and cancellation options could suddenly become commonplace in the most straightforward of agreements.

Ticking your virtual data room checklist

The safest, easiest and most effective way to share documents during a transaction is with the use of a virtual data room (VDR). A good data room is extremely quick to set up, eradicates the need for face-face contact during due diligence and includes flexible, secure and easy to navigate controls.

Now is the ideal time to prepare ourselves for an uptick in activity. As we’ll likely be considering deals requiring a fast turnaround and flexible processes, you might want to consider:

a. Do you have the correct, up-to-date due diligence and supporting documentation

in your VDR to enable a quick turnaround?

b. Have you created a document and index structure that will speed up your

process, taking into account industry and type of deal?

c. Are the permission controls set up, taking into account new considerations such

as staff working from home or taking time off sick? Is each delegated VDR

member aware of their responsibilities and how to work the room’s controls?

d. Have you identified the best possible provider for your transaction? Does that

provider help you save time during your transaction and simplify the M&A process

with easy to use technology and a dedicated 24/7 team? This article highlights

the main questions to ask when selecting your data room.

As deal processes may move increasingly online, the use of VDRs will become even more critical. The advisor/client relationship will undoubtedly be changed by this need to work remotely. So as the need for face-to-face meetings decreases, it’s the optimum time to get ahead of the curve and ensure you have the remote technology and support to work for you.

What else should you be doing today, to prepare for tomorrow?

What else should you be doing today, to prepare for tomorrow?

There is no end date for the Covid-19 pandemic. Our politicians may deem it ‘safe’ for us to leave our homes, to socialise, to eat out again – but how many of us will listen to this, and how many will continue to be struck down by the fear that has been instilled? These basic alterations to human behaviour – a reluctance to travel or to go to a local bar for fear of infection, or to buy new clothes or shoes because of a recent job loss – are here to stay for the foreseeable future.

These socio-economic changes will inevitably change the way in which companies operate, and are bought and sold. But there are ways in which we can prepare ourselves for this ‘new normal’, and for the surge of activity which will come.

Industry players should be prepared for the timing, structures and flows of their deals to be radically different from those seen in recent years. You’ll need to be more flexible, nimble and open to new ways of working than ever before. Now is the time to evaluate where you could cut costs, and where you could implement new procedures to future-proof your business.

Industry players should be prepared for the timing, structures and flows of their deals to be radically different from those seen in recent years.

Use this time to understand how using the right data room to its full potential will make your transactions simple and easier. Avoid delays when normal service is resumed – use today to talk to providers, understand their offering and see how they could help you run smoother transactions.

We are already seeing advisors and principles preparing their data rooms, renewing contracts, refining their due diligence processes and contacting sales reps to get ready for this next stage of growth. Now is not the time to take our foot off the pedal. It’s the time to consider your growth options, ensure that you have the right partners in place, and ensure that you are ready for the next chapter.

We are already seeing advisors and principles preparing their data rooms, renewing contracts, refining their due diligence processes and contacting sales reps to get ready for this next stage of growth.

About EthosData

EthosData is a Virtual Data Room provider, based in London, UK. We’ve been operating for 13 years and have handled 900+ billions in deal transactions. With our intuitive platform and dedicated support team, dealmakers can now focus on their transactions, and leave the data room to the experts.

You can contact us at contact@ethosdata.com

To continue reading on this topic we invite you to read this article from One To One: Why M&A will rekindle after Covid-19 crisis.